If you’re here, you’re likely looking to strengthen your understanding of financial statements and make smarter, more confident investment or business decisions. Financial reports can feel overwhelming, but when you know what to focus on, they become powerful tools for evaluating performance, stability, and long-term potential. This article is designed to break down the essentials in a clear, practical way—so you can move from confusion to clarity.

We’ll walk through the key components of financial reporting, with special attention to cash flow statement interpretation, helping you see how cash actually moves through a business beyond what profits alone may suggest. By combining market insight, economic context, and proven financial analysis frameworks, this guide equips you with reliable, experience-backed knowledge you can apply immediately. Whether you’re analyzing a company, planning investments, or refining your financial strategy, you’ll gain actionable insights grounded in real-world finance principles.

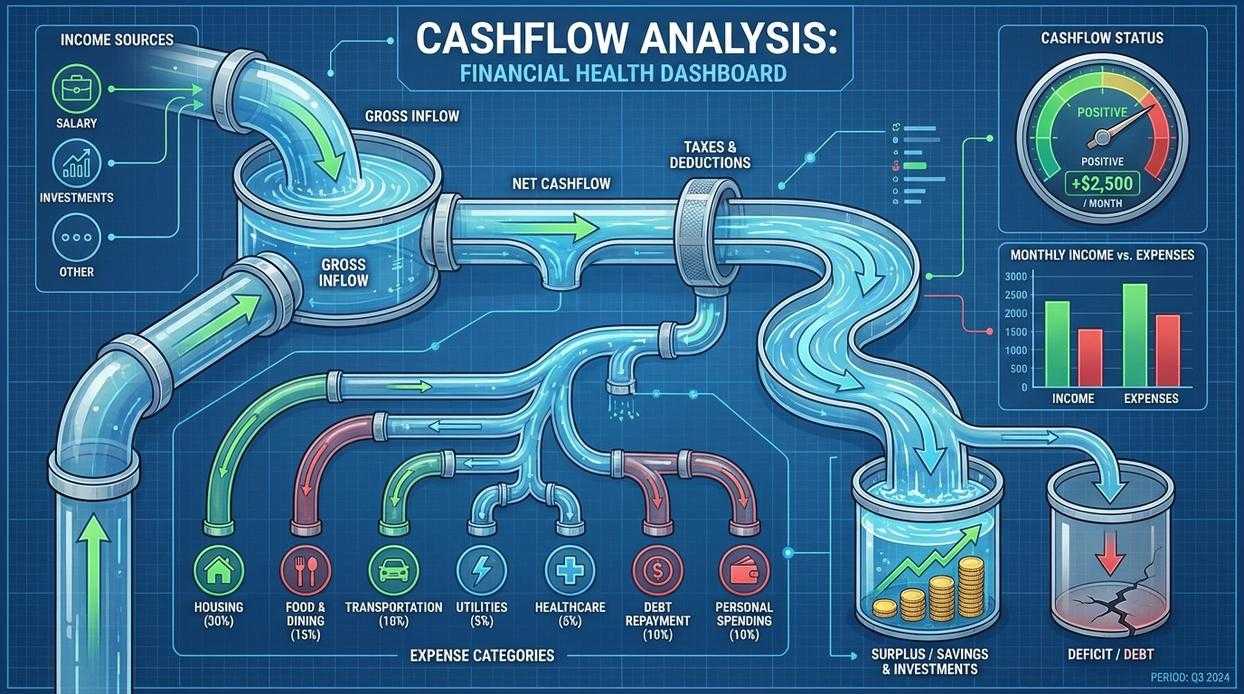

Profits can sparkle on a quarterly report, yet seasoned investors in Singapore or Mumbai know better. Net income bends under depreciation schedules and revenue recognition rules. However, cash pays suppliers in Jurong and salaries in Bengaluru. That’s why cash flow statement interpretation matters. Start with operations: is core business generating steady ringgit or relying on one-off boosts? Next, examine investing outflows for capex versus flashy acquisitions. Finally, scrutinize financing—new debt on the SGX isn’t always growth. Critics argue earnings tell the full story; still, cash exposes reality (no Hollywood accounting twist). Use it to spot red flags early and decisively.

The Three Engines of Cash: Operations, Investing, and Financing

Think of a company’s cash flow like a car with three engines. If one fails, the ride gets bumpy.

Cash Flow from Operations (CFO): The Core Generator

CFO shows cash earned from everyday business activities. In simple terms, it answers: Is the core business actually making money? A consistently positive CFO signals sustainability. For example, if a retail chain reports rising profits but negative CFO, it may be struggling to collect payments (a red flag).

Practical tip: Compare net income to CFO. If profits rise but cash doesn’t, dig deeper into receivables or inventory levels.

Cash Flow from Investing (CFI): The Growth Engine

CFI tracks spending on assets like equipment or property. Negative CFI isn’t always bad—it often means expansion. When Amazon invested heavily in warehouses, CFI was negative, but it fueled long-term growth.

Step-by-step: Check whether asset purchases align with revenue growth trends.

Cash Flow from Financing (CFF): The Capital Structure

CFF shows borrowing, issuing stock, dividends, or buybacks. Heavy debt financing can boost growth—but increases risk if cash slows.

When doing cash flow statement interpretation, analyze all three together. A healthy company often shows positive CFO, strategic negative CFI, and balanced CFF (growth without overreliance on debt).

Key Ratios for Immediate Financial Insight

When I’m sizing up a company, I don’t start with earnings per share. I start with cash. Specifically, I look at four ratios that cut through accounting noise and tell me what’s really going on.

Free Cash Flow (FCF): The Ultimate Health Metric

Free Cash Flow is defined as Operating Cash Flow (CFO) minus Capital Expenditures (CapEx). In plain English, it’s the cash left after a company maintains or upgrades its assets. This is the money available to repay debt, pay dividends, or reinvest for growth. Some argue earnings matter more because they reflect profitability. I disagree. Earnings can be adjusted; cash is stubborn. According to a 2018 study in the Journal of Finance, firms with strong free cash flow generation tend to outperform over time.

Operating Cash Flow Margin: The Efficiency Test

Calculated as CFO divided by total revenue, this ratio shows how efficiently sales turn into cash. A rising margin signals improving operational discipline. If revenue grows but cash doesn’t, that’s a red flag (and yes, it happens more often than you’d think).

Cash Flow to Debt Ratio: The Solvency Check

This measures how well annual operating cash flow covers total debt. Higher is safer. Critics might say low rates make debt harmless. I’d counter that cycles turn quickly, and liquidity dries up fast.

Capital Expenditure Coverage Ratio: The Sustainability Indicator

This shows how many times operating cash flow covers CapEx. If coverage is thin, growth may depend on external financing.

Ultimately, mastering these metrics strengthens your cash flow statement interpretation skills. For a broader breakdown, review key financial ratios every investor should know: https://ftasiafinance.com.co/key-financial-ratios-every-investor-should-know/.

Reading Cash Flow Patterns Like an Insider

In financial hubs from Singapore’s Raffles Place to Hong Kong’s Central district, analysts often start with one thing: the cash flow statement interpretation. Why? Because profit can be polished, but cash is stubbornly honest (and markets in Asia tend to reward honesty).

First, consider The Healthy Grower Profile: Positive CFO, Negative CFI, Negative CFF. CFO (Cash Flow from Operations) reflects money generated from core business activities. CFI (Cash Flow from Investing) tracks capital expenditures or acquisitions. CFF (Cash Flow from Financing) shows debt and equity movements. This pattern signals a company funding expansion internally while reducing debt or rewarding shareholders. Think of a well-established manufacturing firm in Johor reinvesting in automation while buying back shares.

On the other hand, The High-Growth Startup Profile shows Negative CFO, Heavily Negative CFI, Positive CFF. Critics argue this is reckless. However, in sectors like Southeast Asian fintech or EV infrastructure, aggressive reinvestment funded by venture capital is often strategic, not alarming. Grab Holdings, for example, operated this way during expansion (Reuters, 2022).

Now, the real warning sign: The Struggling Company Profile. Negative CFO, Positive CFI, Positive CFF. Selling assets and piling on debt to survive? That’s not strategy—it’s triage. Even seasoned Bursa Malaysia investors treat this as a flashing red light.

Finally, The Mature Dividend Payer Profile: Strong Positive CFO, Neutral/Positive CFI, Heavily Negative CFF. Stable utilities or REITs across Asia frequently fit here, prioritizing dividends over bold expansion.

Ultimately, patterns matter—but context matters more. Industry cycles, regional credit markets, and regulatory shifts can all reshape the narrative.

Investors scanning Asian blue chips on the SGX or HKEX often celebrate rising net income. However, when profits climb while operating cash flow (CFO) shrinks, alarms should ring. This divergence hints at aggressive revenue recognition or stretched receivables—common in property and tech supply chains.

Meanwhile, repeated positive cash flow from financing (CFF) paired with negative CFO suggests the business survives on fresh debt or rights issues. In Southeast Asia’s tighter credit cycles, that’s risky.

Finally, steady inflows from selling plants or stakes—positive CFI—signal distress. Solid cash flow statement interpretation separates durable operators from balance-sheet illusions during volatile regional market downturns.

Early in my investing journey, I celebrated a company’s soaring profits—until it ran out of cash. That sting taught me to look past headlines. Now, I focus on cash flow statement interpretation to see how money truly moves.

In other words, profits can flatter; cash rarely lies.

To move from analysis to action:

- Review operating, investing, and financing flows.

- Compare cash trends to reported earnings.

- Watch liquidity ratios for red flags.

As a result, decisions feel grounded, not hopeful. So before your next investment, pause, follow the cash, and act on financial reality—not accounting theory, with confidence.

Mastering Your Financial Clarity with Smarter Analysis

You set out to better understand what your numbers are really telling you — not just profits on paper, but the real movement of money inside your business or portfolio. Now you can see how cash flow statement interpretation reveals operational strength, liquidity risks, and long‑term sustainability in a way income statements alone never could.

Ignoring cash flow is what leaves many investors and business owners blindsided by shortfalls, stalled growth, or missed opportunities. Strong revenue means little if liquidity is weak. Clear cash insight is what protects your next move.

The next step is simple: start reviewing your cash flow alongside every major financial decision. Compare operating, investing, and financing flows before committing capital. If you want sharper market insight, proven financial frameworks, and trusted Asia-focused economic analysis used by serious investors, explore our latest resources today and apply what you’ve learned immediately.

Clarity drives confidence. Take control of your financial decisions now.

Ask Maritza Wigginsams how they got into global investment strategies and you'll probably get a longer answer than you expected. The short version: Maritza started doing it, got genuinely hooked, and at some point realized they had accumulated enough hard-won knowledge that it would be a waste not to share it. So they started writing.

What makes Maritza worth reading is that they skips the obvious stuff. Nobody needs another surface-level take on Global Investment Strategies, FT-Focused Economic Trends, Finance Planning Techniques. What readers actually want is the nuance — the part that only becomes clear after you've made a few mistakes and figured out why. That's the territory Maritza operates in. The writing is direct, occasionally blunt, and always built around what's actually true rather than what sounds good in an article. They has little patience for filler, which means they's pieces tend to be denser with real information than the average post on the same subject.

Maritza doesn't write to impress anyone. They writes because they has things to say that they genuinely thinks people should hear. That motivation — basic as it sounds — produces something noticeably different from content written for clicks or word count. Readers pick up on it. The comments on Maritza's work tend to reflect that.

Ask Maritza Wigginsams how they got into global investment strategies and you'll probably get a longer answer than you expected. The short version: Maritza started doing it, got genuinely hooked, and at some point realized they had accumulated enough hard-won knowledge that it would be a waste not to share it. So they started writing.

What makes Maritza worth reading is that they skips the obvious stuff. Nobody needs another surface-level take on Global Investment Strategies, FT-Focused Economic Trends, Finance Planning Techniques. What readers actually want is the nuance — the part that only becomes clear after you've made a few mistakes and figured out why. That's the territory Maritza operates in. The writing is direct, occasionally blunt, and always built around what's actually true rather than what sounds good in an article. They has little patience for filler, which means they's pieces tend to be denser with real information than the average post on the same subject.

Maritza doesn't write to impress anyone. They writes because they has things to say that they genuinely thinks people should hear. That motivation — basic as it sounds — produces something noticeably different from content written for clicks or word count. Readers pick up on it. The comments on Maritza's work tend to reflect that.